- Sole Proprietor

- General Partnership -

Chapter 620.81001 FS - For Profit Corporation -

Chapter 607 FS - c-corp vs s-corp

- Not for Profit Corporation -

Chapter 617 FS - Limited Liability Company (LLC) -

Chapter 605 FS - Social Purpose Corporation -

Chapter 607.501 FS - A regular for-profit corporation EXCEPT management protected from shareholder derivitate suits (on account of failure to pursue maximum profits)

- Regular FP corporation except Articles of Incorporation state that it is a "social purpose corporation" as defined in the statute

- Benefit Corporation -

Chapt 607.601 FS - A regular for-profit corporation EXCEPT management protected from shareholder derivitate suits (on account of failure to pursue maximum profits)

- Regular FP corporation except Articles of Incorporation state that it is a "benefit corporation"

- Limited Partnership (LP) -

Chapter 620.1101 FS - Limited Liability Partnerships (LLP) -

Chapter 620.9001 et seq FS - a general partnership were all partners have limited liability

- File a "statement of qualification" saying that the entity is an LLP

- Limited Liability Limited Partnerships (LLLP)

Chapter 620.1102(10) FS - a limited partnership were all partners have limited liability

- To qualify the Certificate of Limited Partnership filed with the State must say that the entity is a limited liability limited partnership

- Professional Associations

Chapt 621 FS - Advantage - protects directors and shareholders from malpractice lawsuits (while leaving the professional alleged to have committed the malpractice exposed)

- Advantage - the entity can receive tax benefits over operating as a sole proprietorship or partnership (example, dedutability of health insurance and other expenses)

- Types

- Professional Association (P.A.)

- Professional Limited Liability Company (PLLC)

- Unlike a corporation, an actions taken by an LLC don't have to be authorized by a board of directors (authority to take actions on behalf of the LLC are governed by the operating agreement)

- LLC Default: There is no tax disadvantage to being an LLC as opposed to a corporation. The IRS, by default, treats LLCs as follow:

- Single Member: By default, the IRS treats a single member LLC as a "disregarded entity"

- Multi-Member; By default the IRS treats multi-member LLCs as partnerships

- Any LLC can elect to be taxed as a corporation (either a "C corp" or an "S corp")

- Corporation Default: Taxation under Subchapter "C" - i.e. "double taxation" (at both the entity and the shareholder level)

- A corporation can elect to be taxed under sub-chapter S

- An LLC's Operating Agreement can authorized one or more of the members to exercise management responsibility OR it can appoint someone to act as "manager". No bylaws, board of directors, or minute book needed

- In contrast, with corporations, a board of directors must first authorize its officers to take specific actions.

- A corporation must allocate its distributions in proportion to each shareholder's ownership share.

- An LLC, on the other hand, does not necessarily have to allocate its profits or losses in proportion to each owner's membership interest. Instead, the distributive share of gains, losses, deductions or credits can be determined in the LLC's operating agreement (and subject to certain IRS restrictions against negative capital accounts).

- Additionally, members of an LLC can transfer and withdraw property into the LLC without the recognition of taxable gain by the LLC or the member with whom the property has been distributed. In the case of corporations, property distributions can result in taxable gain.

- Entrepreneurs hoping to achieve venture seed funding, typically choose to be a corporation taxed under Subchapter C.

- Venture capital firms won't automatically screen out businesses that are not incorporated in Delaware, but they prefer Delaware due to friendly corporate governance benefits and predictable corporate law.

- FOLLOWING FORMALITIES: Not following the formalities allows a court to "pierce the corporate veil" giving creditors access to the personal assets of the owners

- LLCs have fewer formalities (board of director's authorizations etc)

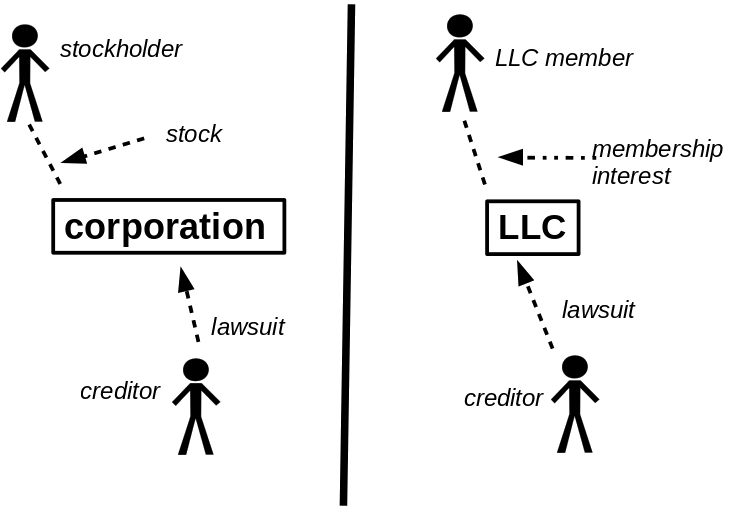

- LLCs and corporations in all states shield members and stockholders from liabilities owed by the entity

- Courts in all states CAN seize corporate stock owned by a judgment debtor

- Courts in All states do not allow the seizure of multi-member LLC membership interests owned by judgment debtors (but they can seize LLC distributions made to those owners)

- Courts in Florida treat single member LLC interests as if they were corporate stock

- Florida Courts can seize single member LLC interests held by a judgment debtor

- Delaware and Wyoming courts treat single member and multimember LLCs the same. Thus, incorporating in those states offer better for assets held by single member LLCs

- Corporations

- In Florida, Wyoming and Delaware the stock held by a judgment debtor can be seized through the courts just like any other asset owned by the debtor

- Multi-Member LLCs

- In Florida, Delaware and Wyoming interests in multi-member LLC are treated as partnership interests and can't be seized (though distributions can be seized)

- Single-Member LLCs

- Florida treats such single member LLC interests as if they were stock in a corporation which can be seized

- Delaware and Wyoming treat single member LLC interests as partnership interests which can not be seized

- Wyoming has a more user friendly on-line incorporation system than does Delaware and some people may not need a lawyer (they would still need a Wyoming registered agent but inexpensive corporate service providers can be found using Google)

- You must pay an annual "franchise tax" to the State of Delaware ($300 per year plus hefty late fees and interest if not timely). - Wyoming has a similar fee but it may be smaller.

- If the Wyoming or Delaware LLC wanted to do business in Florida it would also have to separately pay to register as a "foreign" company with Florida and then pay Florida's annual fee thereafter ($138.75 per year)

- It is unclear how Florida courts will treat foreign single member LLCs with assets in Florida where the protections afforded to the members of those LLCs under Delaware law are being used (arguably) to thwart the interests of the member's Florida creditors.

- Try gaming the system to make an entity appear as if were a multi-member LLC by having a second member with only a minuscule share of the ownership rights & profits with no say in management.

- The law is still relatively new and it is hard to predict if a Florida court would honor such a structure

- Unlike true partnerships the members of an LLC enjoy the same type of limited liability protection that is enjoyed by stockholders of a corporation.

- As a practical matter LLC's often offer better protection from liability than a true corporation because there are far fewer "formalities" that must be complied with (no need for boards of directors, minute books, bylaws, etc).

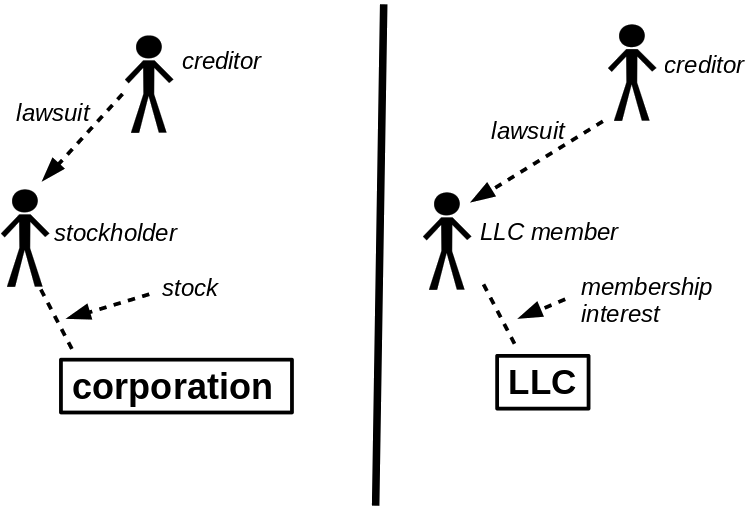

- With true corporations creditors of an owner can get the courts to seize that person's stock in the company (thus giving the creditor full or partial ownership of the company)

- That is not true with multi-member LLCs. Someone with a money judgment against a member can NOT seize that person's membership interest in an LLC. All the creditor can do is get the court to issue a "charging order" seizing any monetary distributions that might (or might not) be made by the LLC to the member.

- Effective January 1, 2024, virtually every legal entity incorporated, organized, or registered to do business in a state must disclose information relating to its owners, officers, and controlling persons with the Financial Crimes Enforcement Network (FinCEN) pursuant to the newly enacted Corporate Transparency Act (CTA).

- It can be used to protect the position of minority shareholders by requiring unanimous approval for important company decisions

- It can regulate the appointment and removal of directors by allowing a shareholder or a group of shareholders each to appoint one or more directors

- It can regulate the raising of capital to avoid the dilution of shareholdings

- It can place restrictions on changes to the nature of the company's business

- It can also provide for the resolution of disputes where a deadlock occurs, through mediation and/or arbitration

List of Other Entity Types

Factors to Consider in Choosing

Between an LLC and a Corporation

Corporate Formalities:

Taxation:

Management Flexibility:

Distributions:

Investment:

Protecting Owners from Creditors of the Entity

Protecting Entity Assets from Creditors of the Owners

Protecting Entity Assets from Creditors of the Owners

BUT

Summary: Protecting Entity Assets from Creditors of the Owners

INCORPORATING IN STATES LIKE DELAWARE OR WYOMING

WILL BE MORE EXPENSIVE THAN INCORPORATING IN FLORIDA

INCORPORATING IN DELAWARE OR WYOMING MIGHT NOT

PROVIDE DESIRED PROTECTION AFTER ALL

SOLUTIONS FOR A FLORIDA LLC?

LLC Limited Liability

(protecting LLC members from creditors of the company)

LLC Limited Liability

(Protecting LLC assets from Creditors of an LLC's member

Corporate Transparency Act

Corporations - Shareholder Agreements

There are many advantages to entering into a shareholders' agreement, including:

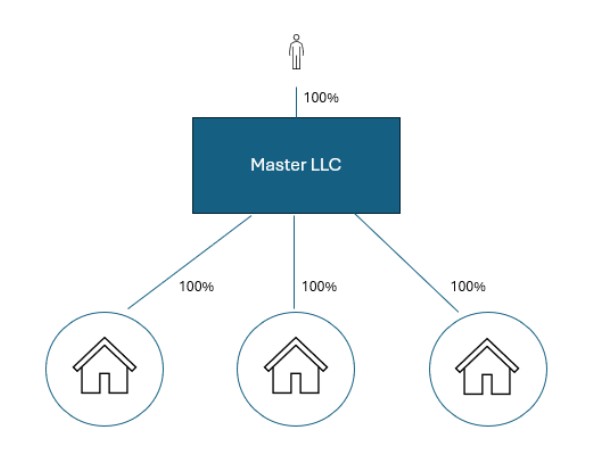

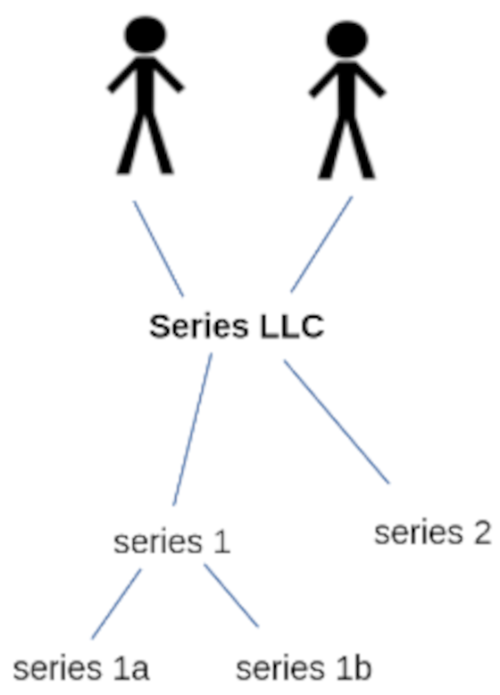

Series LLCs

On June 20, 2025, the Florida legislature authorized Florida LLCs to establish "protected series" Now, an LLC as a single entity, may create one or more separate "series" with that single entity with each series being deemed a separate "Person"

To Qualify as a Series LLC the Entity Must

Create and Maintain Horizontal Shields

This insulation from joint liability and recourse is accomplished by the statutory creation of new "internal" liability shields, also known as "horizontal" shields, which allow for the segregation of assets and liabilities, whereby the "associated assets" and "associated liabilities" of any one series are only available to the creditors of that specific series.

To maintain the new horizontal shields, a Florida series LLC must adhere to strict and clear recordkeeping for the LLC and for each series created by the LLC, whereby the "associated assets" and "associated liabilities" of the LLC, and each series, are maintained contemporaneously and clearly in records and "only if the protected series creates and maintains records that state the name of the protected series and describe the asset with sufficient specificity to permit a disinterested, reasonable individual to:

-

(i) identify the asset and distinguish it from any other asset of the protected series, any asset of the series limited liability company, and any asset of any other protected series;

(ii) determine when and from what person the protected series acquired the asset or how the asset otherwise became an asset of the protected series; and

(iii) if the protected series acquired the asset from the series limited liability company or another protected series of the limited liability company, determine any consideration paid, the payor, and the payee. See Section 605.2301(2)(a)." (emphasis added)

Forms Directory - Nonprofit Corporations

Forms Directory - For-Profit Corporations

Forms Directory - Multi-Member LLCs